US dollar buckled below critcal resistance, eyes on the data

- US dollar in focus on key US calendar week as investors digest Fed rhetoric.

- Fed / ECB convergence under the market's watchful eye.

The US dollar was mixed on the day but remains in the hands of the bears while below 93 the figure as per the DXY.

US stocks held up around record highs overnight, in the wake of the Federal Reserve's Jerome Powell's Powell’s comments from Friday.

Risk sentiment remains elevated but fragile and much will now depend on this week's US data as well as rhetoric from Fed officials as well as from members of the European Central Bank.

Meanwhile, the S&P 500 was up 0.4%, the Nasdaq up 0.9% and the Euro Stoxx 50 up 0.2% proving investors are still relishing the prospects of easy money for slightly longer.

The yield on the US 10-year note was also 2.9bps lower at 1.278%, weighing on the greenback.

US bond yields fell in general as the market is digesting Fed Chair Powell’s comments.

The 2-year government bond yields fell from 0.22% to 0.20%, and 10-year government bond yields fell from 1.31% to 1.28%.

The data is being watched closely and we had our first snippet of such on Monday.

The US Pending Home Sales in July fell 1.8% (vs +0.3% expected), for an annual pace of -9.5%.

The Dallas Fed manufacturing survey fell to 9.0 in August (from 27.3, expected 23.0), continuing to reflect supply chain issues.

With an emphasis on the US jobs market at the Fed, traders were looking to the employment component that fell to 21.9 from 23.7, with wages/benefits at 43.4 from 46.0.

Nevertheless, markets are still going to be digesting Jackson Hole.

Markets had been positioning for an announcement to come as soon as September with expectations of tapering to start in October and concluding in late 1Q 2022/2Q 2022.

However, Jerome Powell merely suggests it “could” be appropriate to begin the taper this year.

He gave no hint as to actual timings and instead explained that the decision-making process would involve a delicate balancing act between the data and the spread of the Delta Covid variant.

The lead into Friday's jobs data may well also be key.

Tuesday's Services PMI, ahead of Wednesday's Manufacturing PMIs as well as the ADP jobs report and then Jobless Claims also have the potential to stir up volatility before Friday's showdown.

''If the outlook changes and the U.S. economy slows significantly, then it would be a likely game-changer for the dollar,'' analysts at Brown Brothers Harriman warned.

''The Fed would have no choice but to adjust its expected tapering path significantly. Yet even then, the dollar may hold up better than expected since a US recession would likely be part of a broader global downturn. It all goes back to relative performances.''

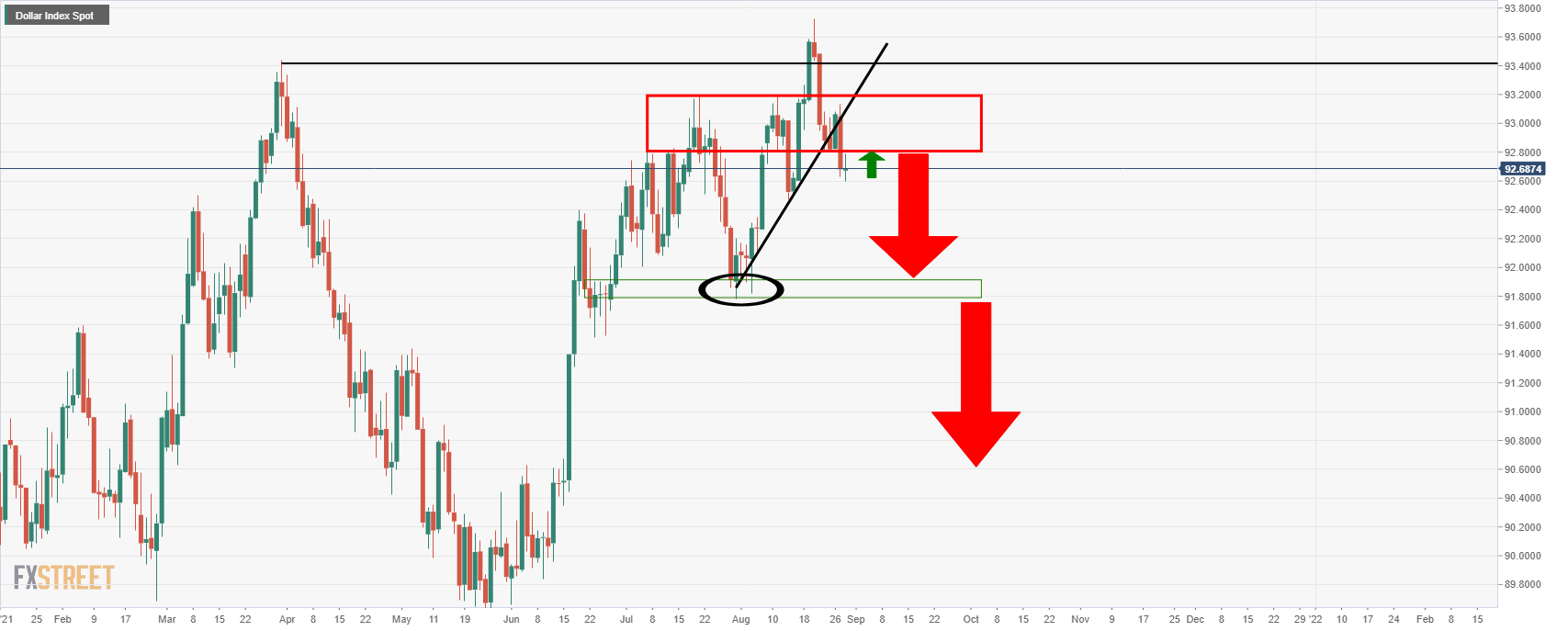

The index is now on track to test the August 13 low near 92.471 with a low on Monday scored at 92.598 so far.

A break below would set up a test of the July 30 low near 91.782:

(Daily chart)

There could be more to go to the downside considering the outcome of the event and how speculators increased their net long US dollar positions in the prior week, according to calculations by Reuters and US Commodity Futures Trading Commission data released on Friday.

The value of the net long dollar position jumped to $8.50 billion in the week ended Aug. 24, compared with a net long of $1.06 billion the previous week.

This was the largest long position since March 2020.

Should the data really disappoint, the DXY could be looking into the abyss from a longer-term perspective:

This would especially be true if the European Central Bank and the Fed be seen to be converging.

ECB’s Philip Lane was concrete at the Jackson Hole, basically, promising to calibrate the QE program to financial conditions BOTH in an upwards and in a downwards direction.

This currently means that the recent new all-time lows seen in EUR real rates could be used as an argument to tone down PEPP-purchases, potentially as soon as September.

Should such sentiment grab the front pages and be construed as the equivalent of a taper, the US dollar would be expected to struggle vs the euro, for which makes up almost 58 per cent (officially 57.6%) of the basket.

Overnight, however, ECB policymaker Francois Villeroy de Galhau said on Monday. downplayed the rise in inflation.

The European Central Bank should take account of a recent improvement in financing conditions in discussing the future of its pandemic-related monthly asset purchases, he said.

Analysts at Westpac explained that and stressed that interest rates will remain favourable, adding that the ECB has more time to decide on the future of the PEPP emergency program than the Fed.

''He did, though, hint at tapering, saying that "on monthly purchase volumes, we are looking at favourable financing conditions, and we should underline that they are more favourable than at our June meeting'.''